Forum

Name : Frankie Time : 11 August 2025 15:43

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : I am pleased to inform you that I passed the examination, and thanks to your guidance.

Name : Terry Time : 16 August 2024 03:14

-

Courses : HKICPA QP Module 11 -

Content : Thanks for your teaching and I passed the paper 11.

Name : Darwin Time : 8 March 2020 13:35

-

Courses : HKICPA QP Module 11 -

Content : Happily share the result of December diet: it's a Pass!. Thank you a lot for your tutoring!

Reply: Time : 08 March 2020 13:46

Name : Ceci Time : 25 August 2019 12:52

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Sir, regarding IFRS9 notes P.97, I do not quite understand why debt instrument measured at FVTPL does not have to calculate the interest income using effective interest method but simply credit it in P/L by using ($100,000 x 5%)? On the contrary, financial liability (P.110) measured at FVTPL would need to add finance cost and reduce interest paid?

Reply: Time : 28 August 2019 00:24

Name : Ceci Time : 24 July 2019 17:00

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Dear Dr. Leung, Regarding IFRS9 financial instrument, notes P.201-203 Illustration 30, would you mind to explain why 30 days and 90days expected loss provision are not taken into account?

Reply: Time : 25 July 2019 11:39

Name : Cherry Time : 14 March 2019 12:09

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Hi Sir, IFRS 9 reclassification of Financial Asset. Changing from FVTOCI to AC, I don't quite understand how to treat the cumulative OCI against the Fair Value on reclassification date. Is that adding-up the cumulative OCI on top of the Fair value?

Reply: Time : 17 March 2019 11:42

Name : Ham Time : 10 February 2019 14:49

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : I've reviewing the Disposal without loss control recently. On Powerpoint P.36, illustration 7 Current NAV of subsidiary is $300,000, Goodwill is $220,000. The question is Parent Transfer 20% share to Sub. and how to deal with it. I see the calculation of Transfer NCI is 20% x ($300,000 + $200,000) My confusion is that NAV of subsidiary is the interest of parent + NCI. By multiplier the whole NAV plus Goodwill to 20%, will the NCI being overlapped or double counted?

Reply: Time : 17 February 2019 10:04

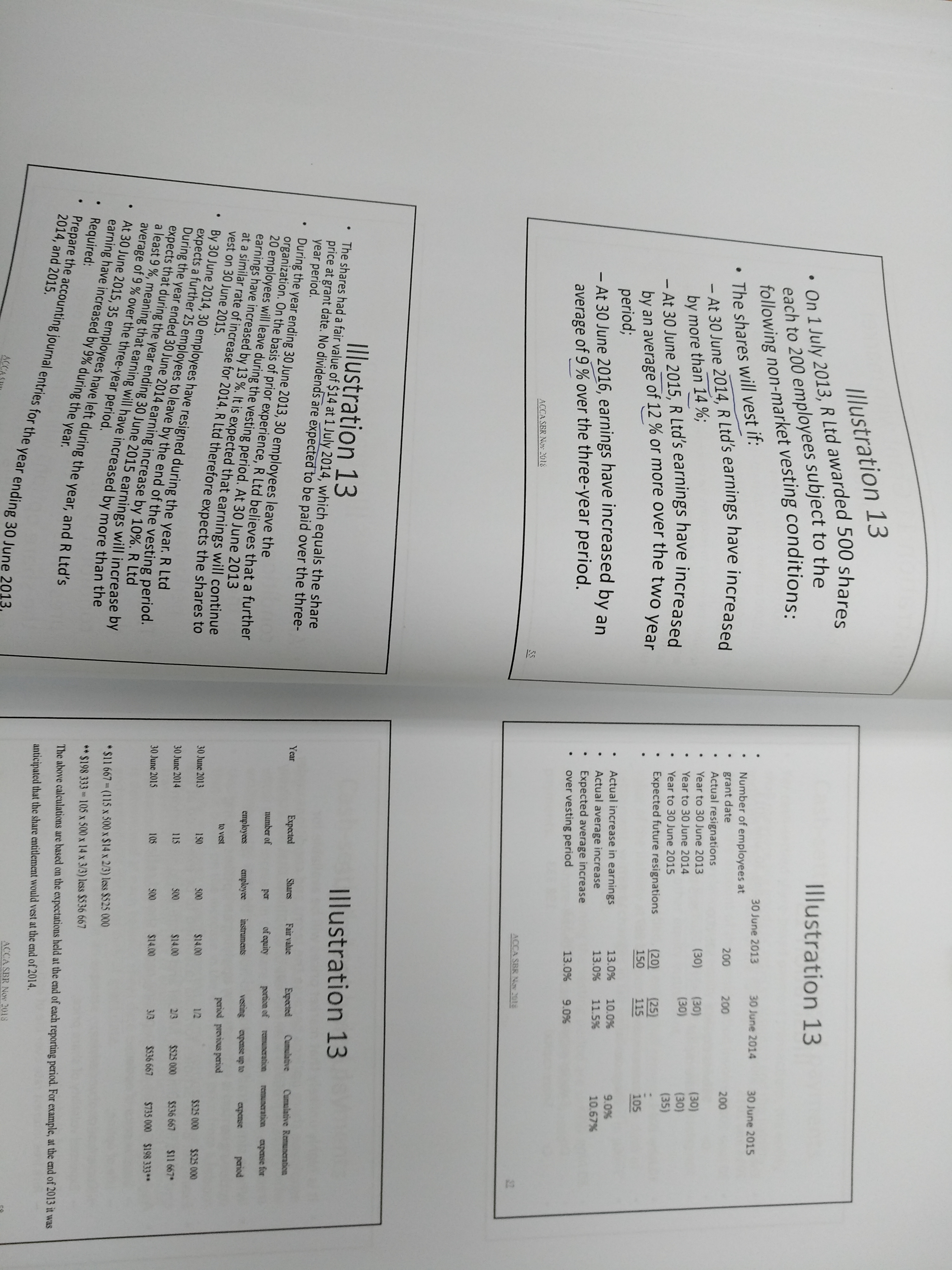

Name : Tino Lo Time : 6 December 2018 23:20

-

Courses : ACCA Professional Examination Preparatory Programme - Strategic Business Reporting -

Content : Hi Mr. Leung, attached is the illustration 13 of Chapter Share based payment. would you please tell me how to figure out the actual average increase in this illustration, 11.5% for 30 June 2014 and 10.67% for 30 June 2015? Thank you

-

Document :  IMG20181206211609.jpg

IMG20181206211609.jpg

IMG20181206211609.jpg

IMG20181206211609.jpgReply: Time : 30 December 2018 22:12

Name : Sham Heung Sang Time : 15 October 2018 16:21

-

Courses : HKICPA QP Module 11 -

Content : Leung Sir, I got it. Many thanks for your help. Regards, Ambrose

Reply: Time : 15 October 2018 23:16

Name : Sham Heung Sang Time : 10 October 2018 18:21

-

Courses : HKICPA QP Module 11 -

Content : Mr. Leung, I am Sham, Heung Sang, your student (just started from 9 Oct 2018), I have not registered a QP student, and so today I tried online registration but failed. Can you let me have a past paper in a short time? My email is ambrose@corporation.com.hk Regards and thanks, Ambrose